Your business misses a payment, and in the blink of an eye, your federal tax refund will be gone. This. Offset Treasury Program Match the overdue SBA balance or disaster loan balance against the amount of money Washington owes you. At the same time Personal Assurance You signed up – thinking your LLC would protect you or allow creditors to target your car, savings, and even your home.

Below you will meet six professional groups that oppose and turn personal responsibility into negotiable numbers.

Why Personal Assurance Turns Business Debt Into Personal Risk

A Personal Assurance Snap a line between your company and your wallet. When you sign a contract, you promise to pay off the debt yourself if the business fails. That promise is common and many mean that the lender may fire you for the entire balance – even if you own a small part of the company.

Under certain terms, your LLC disclaims limited liability. The corporate curtain is gone. Failure to pay and creditors can sue you directly, freeze your bank account or claim your personal assets. Obligations to follow you long after the business closes because it sticks YouNot a unit.

How performance is applied when you miss a payment

Default Rotate the switch. One day you are a customer; Next you are the target.

Be the first to request a ticket and a phone. These warn that the business is in default and remind you that you personally promised to make things right. Many owners ignore the initial warning, hoping for cash flow recovery. That silence often convinces creditors that you do not plan, so the process speeds up.

If the debt is Trader’s Cash AdvanceLenders can freeze your business bank account or deposit UCC debt the same week you defaulted. Loans backed by banks and the SBA are on a slower path, but with more serious consequences. Once the borrower charges the balance, the small business administration can send it to the bank. Offset Treasury ProgramWhich prevents tax refunds and other federal payments.

Here is the usual schedule:

- Day 1: Missed payment; Internal collection begins

- Day 15: Official Letter of Claim for Personal Assurance

- Day 30: MCA Sponsors Can File Confessions of a Judgment or Complaint

- 60–90: Implementation of the initial judgment (debt freezing account); SBA loans move to treasury for offsets

The window between initial claims and legal action is the best time to bring in professional help.

Should you negotiate yourself or call a cavalry?

Some debts are settled by struggle and the provision of reasonable cash. The owners significantly reduced the balance by direct negotiation – giving them a solid dispute letter and preparing all the paperwork.

However, when a lawyer or government collector participates (a lawsuit filed Confession of JudgmentOr Offset Treasury) Game changer. Professional negotiators and attorneys know the minimum of each creditor, where the law sets excessive interest rates, and when to strategically talk about bankruptcy to close a deal.

Quick bowel examination – consider outside help if:

- Debt over $ 25,000

- Judgment appeal or treasury notice has arrived.

- You are facing more than one aggressive creditor.

If you answered yes to these issues, professional help often pays for itself.

How we choose the winner

We have reviewed two companies and have saved only the ones that can be protected or released Personal Assurance In writing. We rate each competitor on a track record of actual results, transparency, fees, the strength of attorneys, client trust and ability to address MCAs, SBA loans, hiring and tax issues.

Here are the top 6 companies:

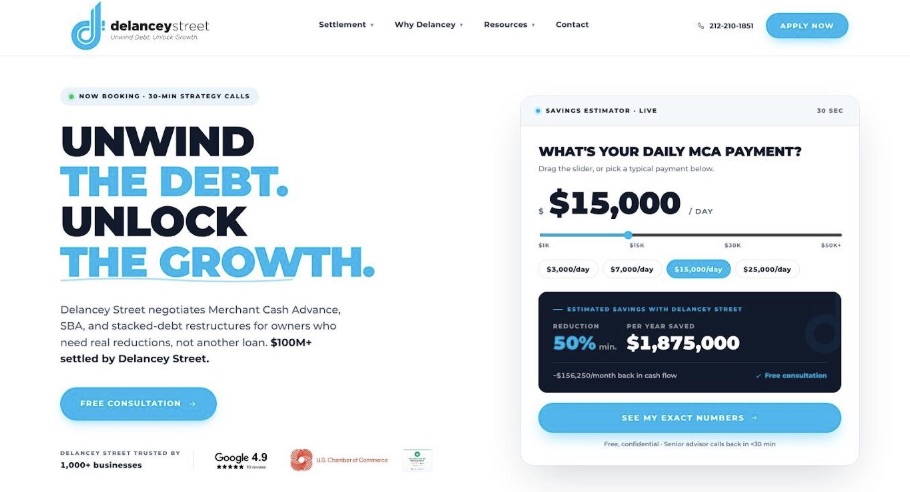

1. Delancey St.: Best Overall for Personal Assurance

Delancey Street focuses on turning personal insurance from a threat into a negotiation chip. The group paired seasonal negotiators with a nationwide network of lawyers. They handle most traders’ cash advances and business loan balances for about 40 to 60 percent Of what you owe and refuse to close the agreement without issuing a written personal guarantee.

Customers never pay in advance. Delancey earns only a fraction of the savings they receive.

Best for: Debt over $ 25,000 with unlimited collateral, especially when a confession, judgment or bank tax claim is on the table.

2. Fight fundraising: Best for debating collection strategies and rebuilding personal credit.

When personal insurance pulls business debt into your personal credit report, the phone calls do not stop and your score will be affected. Combat Collection Expertise in dealing with debt collectors, enforcing debt validation and documenting violations, fair debt collection. They also provide a clear roadmap to rebuild your personal credit after payment.

Best for: Owners whose business debts have already fallen on their own credit and who want to clean up misreporting and rebuild their scores.

3. Perliski Law Group: Best for default SBA loans and treasury payments

When a Small Business Administration submits your 7 (a) balance or EIDL to the Treasury, the normal payment method always fails. Perliski Law Group Explore this federal mountainous area daily. They create offers in mediation that the SBA and Treasury accept and push for debt release instead of endless payment plans.

Best for: SBA or disaster loan deferrals, especially when the Treasury is already paying off a tax refund or debt is crashing into your home.

4. Creditors Assistance: Best for Managing Multiple Businesses – Cash – Pre-stack

Advance funders, merchant cash, move fast. Miss a daily debit and multiple collectors can quickly access your account. Creditors recovery Negotiate directly with the MCA lender and aim to reduce the balance while suspending the aggressive ACH pull over the next few weeks. They work to include personal warranty releases in every payment.

Best for: Many business owners who are playing MCA games need a quick fix before a judgment is entered.

5. CuraDebt: One of the best stop shops when tax issues occur by default

Setting up personal insurance can cause IRS problems because overdue debt in excess of $ 600 is often considered taxable income. CuraDebt Combine debt settlement negotiators with registered agents and tax attorneys under one roof. While a team is working to reduce your balance, the tax entity may prepare a bankruptcy worksheet or continue to offer IRS mediation.

Best for: Owners who settle both business debts and potential tax consequences from the amnesty balance.

6. Second Air Advisor: Best for Reset without Bankruptcy

Some businesses are worth saving – just don’t have the old debt burden attached. Second Air Advisor Use legal strategies such as assignments for the benefit of creditors to transfer valuable assets into new entities, while waiving most legacy debts and personal guarantees.

Best for: Successful business owners who want to avoid personal bankruptcy but need to restructure significant debt (usually $ 500k +).

Work with the company you choose: set the tone and drive the results

Hiring a grant is a partnership. Arrival prepared with all contracts, claims and court documents. During the consultation, ask direct questions: “How successful are clients like me?” And “Will the agreement include the release of a personal warranty in writing?”

Read the engagement contract carefully. The fee schedule should be clear. If a non-legal company requests payment before a settlement is reached, reconsider. When on board, respond quickly to requests and maintain momentum – silence only strengthens the creditor position.

Frequently Asked Questions

Will my personal guarantee affect my credit?

Your score may drop while the account appears to be slow, but usually the damage is temporary. Many owners see their scores recover within a year or two after a settlement – sooner than after bankruptcy.

Can I waive the personal warranty in Chapter 7?

Yes. Chapter 7 can cancel most business liability guarantees, but you can hand over unclaimed assets and carry public records for ten years.

What about the tax bill on the waived debt?

Creditors issue 1099-C for amnesty balances in excess of $ 600. If you go bankrupt when the debt is written off, IRS Form 982 can often exclude that income. Companies like CuraDebt can help with documentation.

Conclusion: Manage reclaims and reinforce

Personal assurance feels concealed until a real professional intervenes. Whether you choose Delancey Street legal pressure, Fight Collections credit protection, Perliski SBA expertise, creditors’ MCA focus, CuraDebt’s debt-plus-tax approach, or Second Wind’s structuring strategy – each street shows the same thing:

Responsibilities are negotiable.

As you act, the balance of energy changes. Suspension of calls, complaints, payments may stop and actual payment offers appear. From there, you can focus on rebuilding credit, strengthening operations, and pursuing your next opportunity.

Entrepreneurs have struggled strategically and returned to strong credit scores and new ventures. You can too.

Choose the approach that suits your situation, move quickly and allow the expert to turn the panic into a plan.